The COVID-19 pandemic inflicted high and rising human costs worldwide, and the necessary protection measures severely impacted economic activity. As a result of the pandemic, the global economy was projected to contract sharply by –3% in 2020, much worse than during the 2008/2009 financial crisis.

In a baseline scenario, which assumed that the pandemic would fade in the second half of 2020 and containment efforts be gradually unwound—the global economy was projected to grow by 5.8% in 2021 as economic activity normalizes, helped by policy support. Because the economic fallout was acute in specific sectors, policymakers implemented substantial targeted fiscal, monetary, and financial market measures to support affected households and businesses domestically.

Internationally, strong multilateral cooperation was essential to overcome the effects of the pandemic, including helping financially constrained countries facing twin health and funding shocks, and channeling aid to countries with weak health care systems (IMF, April 2020).

The global economy grew at 2.9% in 2019, 0.6% lower than the growth registered in 2018 (IMF, 2020). In 2019, the USA economy grew at 2.3% in 2019, 0.6% lower than the growth registered in 2018 where the economy of the United Kingdom grew by 1.4% up from 1.3% in 2018, and that of China by 6.1% in 2019, 0.6% lower than the growth registered in 2018.

In contrast, the global economy grew at 3.6% in 2018, 0.2% lower than the growth registered in 2017 and all advanced economies experienced sluggish growth over the year with exception of the United States of America (USA) (IMF, 2019).

In the UK, the sluggish growth in 2018 and 2019 was as a result of the continuing uncertainty over the ‘No Deal Brexit’, which was passed by the UK in 2020.

China experienced slower growth in 2018 and 2019 compared to 2017 mainly as a result of the trade war with the USA and declining manufacturing output. Some of the factors that led to sluggish growth were addressed in 2020 e.g. a Brexit Deal was reached; US, Mexico and Canada signed a new trade deal code-named USMCA replacing the 25-year old NAFTA. USA and China signed phase one trade agreement in January 2020 and there is optimism that USA-China trade war will soon be fully resolved by signing phase two USA-China trade agreement whereas the USA policy on Iran continues to worsen.

The table below provides a summary of global output growth over the period 2014-2019 and projects for 2020 and 2021.

Summary of Global Output Growth 2014-2021 (% change)

Region/ Country

2014

2015

2016

2017

2018

2019

2020

2021

World Output

3.4

3.1

3.1

3.8

3.6

2.9

-3.0

5.8

Advanced Economies

1.9

1.9

1.7

2.3

2.2

1.7

-6.1

4.5

USA

2.4

2.4

1.6

2.3

2.9

2.3

-5.9

4.7

Euro Area

0.9

1.7

1.7

2.4

1.9

1.2

-7.5

4.7

United Kingdom

3.1

2.2

1.8

1.7

1.3

1.4

-6.5

4.0

Japan

0.0

0.5

1.0

1.8

0.3

0.7

-5.2

3.0

Emerging Markets and Developing Economies

4.6

4.0

4.1

4.7

4.5

3.7

-1.0

6.6

China

7.3

6.9

6.7

6.8

6.7

6.1

1.2

9.2

India

7.2

7.6

6.8

6.7

6.1

4.2

1.9

7.4

Middle East and North Africa

2.7

2.3

3.9

2.5

1.0

0.3

-3.3

4.2

Sub -Saharan Africa

5.1

3.3

1.4

2.7

3.3

3.1

-1.6

4.1

South Africa

1.6

1.3

0.3

0.9

0.8

0.2

-5.8

4.0

Source: IMF, World Economic Outlook, April 2019 and April 2020; 2020 and 2021 are year over year projections.

Since 2014, Africa’s growth has slowed down from a decadal average of 5% to around 3%. This moderate growth continued in 2019, stabilizing at 3.4%, the same as in 2018.

Growth is forecast to pick up to 3.9% in 2020 and 4.1% in 2021(AfDB, 2020). In 2019, East Africa was the fastest growing region, and North Africa continued to make the largest contribution to Africa’s overall GDP growth, due mainly to Egypt’s strong growth momentum. Six African countries were among the world’s 10 fastest-growing economies: Rwanda at 8.7%, Ethiopia 7.4%, Côte d’Ivoire 7.4%, Ghana 7.1%, Tanzania 6.8%, and Benin 6.7%.

For Burundi, the economic recovery strengthened in 2019 (3.3% growth in real GDP) on the back of higher coffee exports, a slight increase in public investment, and a particularly good year for agricultural production. The fiscal deficit rose to 4.2% for 2019, after 3.3% in 2018, mainly due to an increase in recurrent expenditures that was not offset by good performance in tax collection. The deficit has been financed through increased recourse to central bank advances and the accumulation of domestic payment arrears. The risk of debt distress remains high (63.5% of GDP in 2019 compared with 58.4% in 2018) because of increased domestic debt. In inflation, the fall starting in 2018 (from 16.1% in 2017) continued in 2019, with a rate of –3.1% (food prices dropped almost 11%).

Real GDP grew by an estimated 5.9% in 2019, driven by household consumption and investment on the demand side and services on the supply side (such as public administration, information technology, finance and insurance, and transport and storage). GDP was down from 6.5% in 2018, caused mainly by unfavorable weather and reduced government investment. At 5.2%, inflation remains within the central bank’s 5 ± 2.5% target band.

Real GDP of Rwanda was estimated to grow at 8.7% in 2019, higher than the regional average. Growth was mainly in services (7.6%) and industry (18.1%), particularly construction (30%). Investment drove growth, led by public investment in basic services and infrastructure. Real GDP per capita increased 6.1% in 2019. Inflation moved up slightly to 1.6% in 2019, driven by increased domestic demand.

Real GDP growth of South Sudan was an estimated 5.8% in 2019, a large increase from 0.5% in 2018. The 2019 rebound was driven mainly by reopening some oil fields, including those in Upper Nile state, and resuming production, and by the peace agreement signed in September 2018. The oil sector remains the key driver of the economy, followed by services and agriculture. Inflation fell to 24.5% in 2019 from 83.5% in 2018 due to reduced financing of the fiscal deficit.

Real GDP growth of Tanzania was estimated at 6.8% in 2019, down slightly from 7% in 2018. A markedly diversified economy, characterized by robust private consumption, substantial public spending, strong investment growth, and an upturn in exports underpinned the positive outlook. Tourism, mining, services, construction, agriculture, and manufacturing are notable sectors. Growth is projected to be broadly stable at 6.4% in 2020 and 6.6% in 2021, subject to favorable weather, prudent fiscal management, mitigation of financial sector vulnerabilities, and implementation of reforms to improve the business environment. Inflation fell to an estimated 3.3% in 2019 from 3.6% in 2018 due to an improved food supply.

The Ugandan economy reported strong growth in 2019, estimated at 6.3%, largely driven by the expansion of services. Services growth averaged 7.6% in 2019, and industrial growth 6.2%, driven by construction and mining. Agriculture grew at just 3.8%. Retail, construction, and telecommunications were key economic drivers. Inflation is expected to remain below 5%, strengthening the domestic economy.

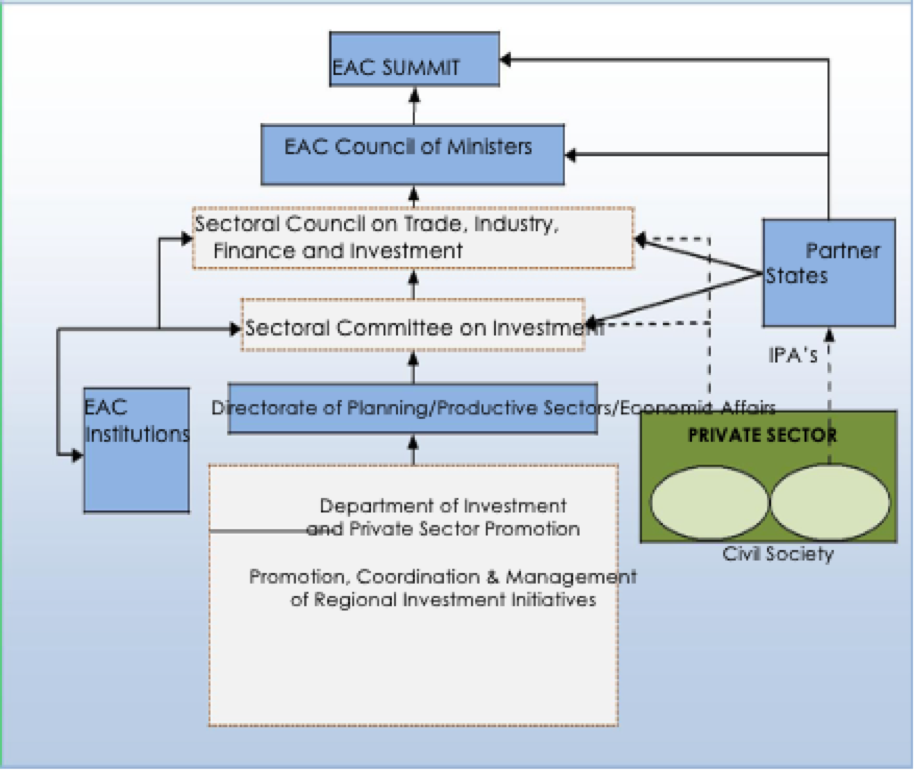

The EAC institutional framework is responsible for investment promotion and creating a conducive investment environment for current and future investors. The Sectoral Committee on investment acts as the technical arm and guides investments in the Community. The stakeholders with regard to the EAC Investment Promotion and Initiatives include:

The EAC Organs (Summit, EAC Council of Ministers and EAC Secretariat), and Sectoral Council on Trade, Industry, Finance and Investment shall be involved in identification, approval, implementation and monitoring of regional investment projects.

EAC Secretariat-Department of Investment and Private Sector Promotion (I&PSP). This department will set up a Regional Investment Promotion Office to coordinate regional investments. The main task of the Regional Investment Promotion Office will be to promote regional investment initiatives in partnership with the National Investment Promotion Agencies (IPAs). IPAs shall designate staff to work with the regional office on regional investment initiatives. EAC Investment Guide Online version shall be part of the EAC web portal i.e. www.eac.int/investment-guide and it shall be updated using information/ data from publications/ documents at national, regional, continental and global levels recognised/ authenticated by the EAC. The mandate to update the EAC investment Guide shall be vested in the EAC Secretariat-Department of Investment and Private Sector Promotion (I&PSP).

The Partner States Governments: The National Investment Promotion Agency (IPA) in addition to promoting and supporting national investments, will provide services under the EAC Regional Investment Promotion Office to investors that want to invest in more than one Partner State or already have investments in more than one Partner State.

The East African Court of Justice will ensure adherence to the law in the interpretation and application of compliance with the EAC Treaty, protocols and other legislations. It will also handle investment arbitration matters.

The East African Legislative Assembly will support regional investment initiatives through legislating on enabling laws and providing oversight over regional investment initiatives.

EAC Institutions. The East African Community Competition Authority (EACA), shall promote and protect fair trade and ensure consumer welfare in the community pursuant to EAC Competition Act (2006). The East African Development Bank will offer structured financial products and services to organisations in the health, education, hospitality and tourism, infrastructure development, energy and utilities, and agriculture sectors. The East African Health Research Commission will coordinate and map out a regional agenda on health research as well as the translation of its results into policy and practice within the Partner States as regards investment initiatives in health sector. The East African Science and Technology Commission will assist in coordination of the development and implementation of Science, Technology and innovation investment initiatives. The Inter-University Council for East Africa will coordinate the harmonization of higher education and training systems in East Africa, facilitate their strategic development and promote internationally comparable standards and systems to ensure high quality human capital development necessary for developing and implementing investments.

Private sector: include private sector representative organisations, East African Business Council (EABC) and other regional private sector apex institutions and will play a lead role in investment identification, promotion, selection, planning, execution, monitoring and evaluation.

Non-state actors: including academic institutions, financial institutions, Civil Society organisations that include trade unions, political leaders, community groups, employee union, community groups, environmentalists and public in general will support EAC regional Investment initiatives through promotion, research monitoring and evaluation, dissemination of information in order to increase impact of regional investments.

Institutional Framework for Investment Promotion, Coordination & Management

Investment provisions in the EAC Customs Union Protocol consist of rules on pre and post-entry treatment, investment incentives, competition and dispute settlements etc. On the other hand, Article 29 of the Common Market Protocol requires Partner States to protect cross-border investments and investment returns of investors of other Partner States within their territories and a schedule for removal of existing restrictions on the free movement of capital within the EAC region.

The proposed EAC Investment Policy 2019-2024 intends to unlock the constraints by putting in place a common legal and regulatory framework for the collective promotion of EAC as a single investment destination. The EAC Investment Policy 2019-2024 will pursue a coordinated region-wide approach to the promotion of investment opportunities seeking to attract domestic, regional and foreign direct investment. This is to complement nationalistic efforts that have been targeting and competing for the same investment catchment areas (source investments markets) at substantial cost to the Partner States themselves. The EAC investment policy will enable the Community to meet its investment targets, particularly in light of the current difficult global economic realities.

The EAC Treaty requires Partner States to "harmonise and rationalise investment incentives, including those relating to taxation of industries".

The EAC Common Market Protocol provides for freedom of movement of goods, labour, services, and capital. Its provisions on investment call for the protection and harmonization of tax regulations. A Policy on EAC Domestic Tax Harmonization was developed and endorsed by the Finance Ministers during the 8th Meeting of the Sectoral Council on Finance and Economic Affairs held in May 2018. Detailed harmonization proposals for VAT and excise taxes rates were being developed for consideration by the finance ministers. The 2006 EAC Model Investment Code provides for the free transfer of assets, and protection from uncompensated expropriation. EAC countries can negotiate and enter investment treaties with third countries. A Model Investment Treaty was adopted in 2016, with the objective of guiding, and serving as a template for, negotiations.

The EAC investment Framework supports free movement of people, capital, labour, services and right of establishment and residence; promotes balanced and competitive industrial/manufacturing sector in the region; promote participation of the citizenry and having them fully aware of the EAC affairs; strengthens relations with other regional and international organisations; supports duty Drawback Schemes; supports Duty and VAT Remission Schemes; supports Manufacturing-Under-Bond (MUB) Schemes; provides for Export Processing Zones (EPZ); provides for the establishment of free ports within the EAC; and provides for Harmonisation of Duty Exemption Regimes.

On the other hand, double taxation remains a major hurdle for cross-border investment flows. Investment income generated from cross-border operations are taxed not only in the country of generation, but also in the country of residence of the taxpayer. An Agreement on the Avoidance of Double Taxation was signed in November 2011, but the ratification process is ongoing (EAC, 2016, The Double Taxation Avoidance Agreement of the East African Community Handbook). The ratification process is slow due to fears of loss of revenue and tax evasion. So far, Kenya, Rwanda and Uganda had ratified the Agreement.

Furthermore, the EAC Partner States have their own institutions and regulatory mechanisms for dealing with foreign investment. Each country has its own requirements with respect to such matters as company registration and incorporation procedures, permits and licenses, property acquisition, access to capital and land, ownership and management control, and exit procedures.

The EAC Customs Union Protocol furthers the liberalisation of intra-regional trade in goods; promotes production efficiency in the Community; enhances domestic, cross-border and foreign investment; and promotes economic development and industrial diversification; Trade Facilitation - The Partner States have agreed to cooperate in simplifying, standardising and harmonising trade information and documentation so as to better facilitate trade in goods.

The Customs Union Protocol spells out the rules and regulations that are to govern trade within and outside the Community. The areas of cooperation in the Customs Union are:

Customs administration;

Matters concerning trade liberalisation;

Trade related aspects including the simplification and harmonisation of trade documentation, customs regulations and procedures;

Trade remedies;

National and joint institutional arrangements;

Training facilities and programmes on customs and trade;

Production and exchange of customs and trade statistics and information; and

The promotion of exports.

The key pillars of the EAC Customs Union are the Common External Tariff; the EAC Rules of Origin; and the Customs Management Act, 2004.

The EAC Common External Tariff (CET)

With effect from 1st July, 2022 the EAC Common External Tariff (CET) will be structured under four bands of:

0% for raw materials and capital goods;

10% for intermediate goods not available in the region;

25% for intermediate goods available in the region; and

35% for imported finished products available in the region

The EAC Customs Management Act, 2004

The EAC Customs Management Act, 2004 governs the administration of the Customs Union, including legal, administrative and operational matters.

The Directorate of Customs under the EAC Secretariat identifies policy issues and coordinates and monitors customs and trade-related activities in the EAC.

The Community has developed anti-dumping regulations, as elaborately highlighted in the EAC Customs Union Protocol.

EAC Single Customs Territory (SCT)

The EAC Single Customs Territory (SCT) came into effect in 2014. Implementation of the SCT is aimed at improving trade facilitation through the introduction of ‘hard and soft infrastructure', which facilitate the interconnectivity of customs systems to facilitate seamless flow of information between customs stations and a payment system to manage transfers of revenues between EAC Partner States.

The Single Customs Territory has been implemented to facilitate faster clearance and improvement in cargo movement along the two corridors (Northern and Central) and the now Standard Gauge Railway line.

The implementation of the SCT has witnessed the development of requisite instruments, the information Technology has been revamped to respond to the new operating environment and the capacity of both the public and private sectors equally enhanced to facilitate the smooth rollout of the SCT.

There has been increased trade and investment in the EAC as a result of elimination of non-tariff barriers based on an online monitoring and tracking system, improved infrastructure like the One Stop Border Posts (OSBP), introduction of the Integrated Border Management (IBM) and use of Information, Communication and Technology (ICT).

Standardisation, Quality Assurance, Metrology and Testing (SQMT)

Under Article 81 of the Treaty Establishing the Community, the EAC Partner States recognised the importance of standardisation, quality assurance, metrology and testing (SQMT) for the promotion of trade and investment and consumer protection, among other things.

Non-Tariff Barriers (NTBS)

Under Article 13 of the Customs Union Protocol, the EAC Partner States have agreed to remove all existing non-tariff barriers to trade and not to impose any new ones. Also, Re-exports are exempted from the payment of import or export duties.

EA Competition Policy

The Community also put in place an EAC Competition Policy and Law with an aim to deter any practice that adversely affects free trade within the Community. Its implementation agency, the EAC Competition Authority, deals with all competition issues having cross-border effects. In principle, domestic competition issues remain under the jurisdiction of national competition laws and institutions.

Trade Agreements

The EAC has increased market access to EAC goods and services by entering into a number of key trade agreements such as;

the Tripartite Agreement between the EAC, SADC and COMESA to establish a Tripartite Free Trade Agreement (TFTA);

the US-EAC Trade and Investment Agreement; and

the Economic Partnership Agreement (EPAs) aimed at the formation of a free trade area between the EAC and the European Union (EU) which has been signed by two Partner States, i.e. Republics of Kenya and Rwanda.

EAC Partner States have also ratified the African Continental Free Trade Agreement (AfCFTA) that will integrate the EAC regional economy into the African continental trade and bring about sustainable trade and investment opportunities and unleash the region’s growth potential.

The EAC has put in place sufficient legal framework that has created a conducive legal environment for investments to thrive. This legal framework is enabling EAC Partner States to cooperate in the areas of Investment and Industrial Development to harness the investment potential to promote economic growth and development in the region.

The legal framework is also enabling harmonisation and rationalisation of investment incentives with a view to promoting the EAC as a single investment area. It is also enabling efficiency in production. This EAC legal framework is provided for in: the EAC Treaty Articles, 79-80 and 127-129; The EAC Customs Union Protocol, Article 3 (c) and (d); The EAC Customs Management Act Article 25; The EAC Competition Act; the EAC Common Market Protocol Articles 23 and 29; and The EAC Model Investment Code 2006.

The legal framework of the EAC

Act

Status

Treaty and Protocols

Treaty for the Establishment of the EAC

Signed in 1999, in force since 2000

Protocol on the Establishment of the EAC Customs Union

Signed in November 2004, in force since January 2005

Protocol on the Establishment of the EAC Common Market

Signed in November 2009, in force since July 2010

Protocol for the Establishment of the EAC Monetary Union

Signed in November 2013, in force since 2014

Legislation

The EAC Customs Management Act, 2004

Last amendment in 2012, in force

The EAC Elimination of Non-Tariff Barriers Act, 2017

In force - not ratified

The EAC One Stop Border Posts Act, 2016

In force

The EAC Vehicle Load Control Act, 2013

In force

The EAC Civil Aviation Safety and Security Oversight Agency Act,2009

In force

The EAC Competition Act, 2006

Last amendment in 2009, in force since December 2014

The EAC Trade Negotiations Act, 2008

In force (in the process of being repealed)

The EAC Standardization Quality Assurance Metrology and Testing Act, 2006

In force

EAC Investment Policy 2019-2024

Still in draft form

Source: Trade Policy Review of the EAC by WTO, 2019 and EAC Secretariat

Rationalising investments and the full use of established industries to promote efficiency in production, as well as harmonising trade policies, investment incentives and product standards, with a view to promote the Community as a single investment area.

Providing an enabling environment for the private sector to take full advantage of the Community through the promotion of a continuous dialogue with the private sector to help create an improved business environment and enhancing investor confidence in the region.

The EAC institutional framework is responsible for investment promotion and creating a conducive investment environment for current and future investors.

For the EAC priority investor sectors/ areas, the project profiles are provided in the table below.

EAC Investment Sectors and Project Profiles

S/N

Sector

Project Profiles

1.

Agriculture and agribusiness

Undertaking large-scale commercial farming of crops such as sugarcane, rice, wheat, coffee, tea, sunflower, pulses, floriculture, cotton, sisal, grape, simsim, maize, potatoes, beans, peas, cassava and soya

Development of improved seeds, fertilizer, pesticides, herbicides, crop processing, and farm equipment

Manufacture of grain mill products, starches and starch products and prepared animal feeds

Manufacture of other food products (e.g. bread, sugar, chocolate, pasta, coffee, nuts and spices)

The manufacture of bottled and canned soft drinks, fruit juices, beer, and wines

Sugarcane farming and sugar production

Establishing fish processing plants and modern fishing boat building yards

Food and beverages manufacturing including manufacturing, processing, and preservation of meat, fish, fruit, vegetables, oils and fats

Deep Sea Fishing (snappers, emperors, tuna, sword fish, marlin, king fish and sailfish)

Value addition in fish and other fisheries products, cold chain, manufacturing of fishing gear and accessories

Establishment of commercial fish cage culture in both marine and freshwater areas

Agro-industries and agro-processing to add value to agricultural, livestock, forestry and fisheries products

Establishment of dairy farms and facilities for processing/ manufacturing of dairy products

Establishment of ranches (cattle, sheep and goats) and farms (poultry and piggery) and investment in Livestock farming focusing on Beef, Dairy, Chicken, Hides and Skins

Establishment of modern slaughtering facilities and processing plants

Establishment of breeders’ farms for grand and parent stock

Establishment of animal feeds processing plants

Establishment of commercial layers and broiler farms and establishment of broiler processing plants

Establishment of tanneries, production of footwear and leather goods

2.

Infrastructure

Development of the Dar-es-salaam- Isaka-Kigali railway project, which will connect Kigali (Rwanda) from Isaka to the Tanzanian port of Dar es salaam.

Development of Mombasa–Nairobi-Kampala-South Sudan-Kigali standard gauge railway line

Transport corridors

The Northern Corridor from Mombasa to Bujumbura is part of the Trans-African Highway (Mombasa - Lagos) while the Tunduma - Moyale road is part of the Cape to Cairo Highway

There are two transit corridors that facilitate import and export activities in the region: - The Northern Corridor (1,700 km long) commencing from the port of Mombasa and serves Kenya, Uganda, Rwanda, Burundi and Eastern DRC. - The Central Corridor (1,300 km long) begins at the port of Dar es Salaam and serves Tanzania, Zambia, Rwanda, Burundi, Uganda and Eastern DRC.

The five major transport corridors are: - Mombasa - Malaba - Kigali – Bujumbura - Dar es Salaam - Rusumo with branches to Kigali, Bujumbura and Masaka - Biharamulo - Sirari - Lodwar – Lokichogio - Nyakanazi - Kasulu - Tunduma with a branch to Bujumbura - Tunduma - Dodoma - Namanga - Isiolo – Moyale Roads:

Establishment of communications infrastructure and services

3.

Manufacturing

Establish motor vehicle and motorcycle assembly and manufacturing plants and spare parts production facilities

Establish computer assembly and manufacturing facilities

Establish mobile phone assembly and manufacturing facilities

Establish Textile, Apparel, and Beauty Products Industries

Establish Cosmetics and fragrances industries

Manufacture of electronics

Manufacture of chemicals

Production of Pharmaceuticals

Manufacture of medical appliances and equipment

Manufacture of metals and engineering products

Manufacture of machinery and machine tools

Manufacture solar panels for rural electrification

Production of furniture, construction, and building materials

Manufacture of steel

Manufacture of glass and plastics

Establish lighting industry

Establish glass and plastic products industry

Establish ceramics industry

Establish packaging industry

4.

Energy

Generation of energy from biogas, hyrdocarbons (natural gas, oil, and coal), uranium and renewable resources including eneration of energy from solar and wind

Extraction of biofuels – Ethanol from sugar; Biodiesel from palm oil and jatropha

Geothermal exploration and development

5.

Mining and metals

Processing of minerals

Processing of precious metals and gemstones

Production of iron ore and steel

Extracting and processing of minerals such as nickel and uranium

Investment in minerals smelters

6.

Oil and gas

Production of Liquefied Natural Gas (LPG)

Manufacturing of Liquefied Natural Gas (LPG) cylinders, valves and regulators, installation of filling plants

Establishment of processing plants and industries for the production of refined mineral oil, petroleum jelly and grease, fertilizers; bituminous based water / damp proof building materials e.g. roofing sheets, floor tiles, and tarpaulin

Establishment of chemical industries e.g. distillation units for the production of Naphtha and other special boiling point solvents used in food processing

Development of petrochemicals industries

Large scale production of chemicals and solvents e.g. chlorinated methane, Formaldehyde, Acetylene etc. from natural gas

7.

Tourism

Establishment of resort cities

Branding of premium parks

Construction of new internationally branded hotels in major cities/ towns and game parks

Development of high-quality Meetings, incentives, conventions and exhibitions (MICE)tourist facilities and conference tourism facilities

Provision of air/ground transport

Development of Beach tourism, cultural, historical sites, and eco-tourism facilities

Health tourism

Sports tourism

8.

Education, research and innovation

Establishment of specialised education, research and innovation institutions to address specific regional human capital requirements and research and innovation needs of the region

9.

Health

Establishment of specialised hospitals and diagnostic centres of international standing

Establishment of specialized medical facilities of international standing

The EAC priority investor sectors/ areas include agriculture and agribusiness; infrastructure; manufacturing; energy; mining and metals; oil and gas; tourism; education, research and innovation; and health.

Agriculture and agribusiness:

Agriculture is still the backbone of the EAC economy and is the number one employment sector. The sector also contributes greatly to GDP growth. Agriculture remains central to the industrialization of the EAC as it provides markets for industrial products and raw materials for industries, especially the agro-processing sector. The region has millions of hectares of arable land suitable for agricultural mechanisation and irrigation. The investment opportunities include commercial farming, deep-sea fishing, agro-processing, value addition in agriculture, livestock, fisheries, and forestry products.

Infrastructure:

Infrastructure is one of the most critical enablers of successful regional integration, taking into account its importance in facilitating activities such as trade, agriculture, tourism, and the movement of labour and other resources. Thus, the EAC recognises that regional infrastructure interventions are key to attracting investment into the region, improving competitiveness, and promoting trade. The sector has the following sub-sectors: Roads; Railways; Aviation; Communications and Inland waterways. The infrastructure and support services sub-sector covers roads, railways, civil aviation, maritime transport and ports, multi-modal transport, freight administration and management. The EAC operates 5 modes of transport systems consisting of road, rail, maritime, air transport and oil pipeline. Public-Private Partnership (PPP) opportunities exist in intra-EAC road and railway networks as well in Airports and Port projects

Manufacturing:

Manufacturing is a key sector in EAC’s economic development, both in its contribution to the regional output and exports, and for job creation. Emphasis in the EAC Partner States is on setting key targets and specific goals to steer industrial growth including the development of Special Economic Zones, Export Processing Zones, industrial parks and clusters, and niche products. There are a wide range of direct and joint-investment opportunities in this sector, including agro-processing, garments, the assembly of automotive components and electronics, plastics, paper, chemicals, pharmaceuticals, metals and engineering products for domestic and export markets. Also, the region offers abundant natural resources which provide plenty of raw materials for the manufacturing industries such as cotton for garment and textile industries, sisal for canvassing, iron for steel, as well as various minerals and gemstones.

Energy:

EAC is endowed with diverse energy sources including hydro, biomass, natural gas, coal, geothermal, solar and wind power and uranium, much of which is untapped. Investment opportunities exist in generation of energy from biogas, hydrocarbons (natural gas, oil, and coal), uranium and renewable resources; generation of energy from solar, wind; extraction of biofuels; and geothermal exploration and development.

Mining and metals:

Mining has placed EAC in the higher ranks of African economies in terms of attracting FDIs. EAC is endowed with a variety of industrial minerals and precious metals as well as gemstones.

Oil and Gas:

South Sudan has huge oil deposits and huge quantities of oil were recently discovered in Uganda, Kenya, and Tanzania. Oil exploration is ongoing in the EAC Partner States. In Tanzania, there have been several gas discoveries on the coastal shore of the Indian Ocean at Songo songo, Mnazi bay, and Mkuranga in the Coast Region. These discoveries are catalysts of natural gas developments in Tanzania. The EAC region is becoming an oil and gas hub that is presenting a lot of investment opportunities and attracting a lot of FDIs. Most opportunities are in exploration and extraction.

Tourism:

Tourism is one of EAC’s most important industries and has strong linkages with transport, food production, retail, and entertainment. EAC is still one of the most popular tourist destinations and has many investment opportunities in the tourism sector. The investment opportunities include the establishment of resort cities; branding of premium parks; construction of internationally branded hotels; Development of high-quality Meetings, incentives, conventions and exhibitions (MICE) tourist facilities and conference tourism facilities; and health and sports tourism.

Education, Research, and Innovation:

Higher Education Institutions (HEIs) in the EAC have never been ranked among the top 300 HEIs globally. EAC achieving its social and economic development objectives is largely dependent upon its most valuable resource – its people. Yet the research and innovation output is still low and needs to be improved if the region is to graduate to lower middle income status. The investment opportunities in this sector are in establishment of specialised education, research and innovation institutions to address specific regional human capital requirements and research and innovation needs of the region. Regional innovation ecosystems are grossly lacking and need to be established in partnership with the private sector.

Health:

The EAC Heads of State considered and approved the following health investment priorities in the health sector:

expansion of access to specialized health care and cross border health services;

strengthening the network of medical reference laboratories and the regional rapid response mechanism to protect the region from health security threats including pandemics, bio-terrorism and common agents;

expansion of capacity to produce skilled and professional work force for health in the region based on harmonized regional training and practice standards and guidelines;

increase access to safe, efficacious and affordable medicines, vaccines, and other health technologies focusing on prevalent diseases such as malaria, TB, HIV/Aids, non-communicable diseases (NCDs) and other high burden conditions;

upgrading of health infrastructure and equipment in priority national and sub national health facilities / hospitals;

establishment of strong primary and community health services as a basis for health promotion and diseases prevention and control;

expansion of health insurance coverage and social health protection;

improvement of quality of healthcare, health sector efficiency and health statistics; and

The priority areas for investment in EAC Partner States are provided in the table below. It also provides priority investment areas for EAC consistent with the investment priority areas in the Partner States.

The EAC Investment Priority areas were selected giving priority to those with a high potential for regional value chains.

Priority Areas for Investment in EAC

Burundi

Agriculture including fisheries and livestock

Mining and Energy Sector

Manufacturing/ Processing Industry

Advanced maritime transportation Construction of modern tourism infrastructure

Kenya

Food Security,

Affordable Housing,

Manufacturing

Affordable Health care,

Energy

Financial Services

Information Communication Technology (ICT)

Agriculture

Infrastructure

Rwanda

Manufacturing

Agro-processing

Tourism

Real estate and construction

Information Communication Technology (ICT)

Services

Mining

Infrastructure

Energy

Education

Health services

South Sudan

Agriculture, livestock and fisheries

hard and soft infrastructure

Mining

Agri-business

Energy

Tourism

Uganda

Agriculture and agribusiness

Mineral beneficiation

Tourism

Packaging

ICT

Oil and gas

Renewable energy

Manufacturing

Infrastructure

Services

Tanzania

Manufacturing

Agriculture, Livestock and Fisheries

Mining and Metals

Tourism

Services/ ICT

Economic Zones

Economic Infrastructure

Energy

Real Estate

Oil and Gas

Financial Services

Telecommunication Broadcasting

Zanzibar

Industrial manufacturing or assembling

Up market tourism

Agriculture and fisheries

Real-estate development

Energy

Infrastructure development

Information Communication Technology (ICT)

EAC

Agriculture and agribusiness

Tourism

Infrastructure

Manufacturing

Mining and metals

Energy

Education, research and innovation

Health

Oil and Gas

Source: Investment (Promotional) Code Acts and Investment Promotional Agencies Websites of Partner States.